LHDN Section 33(1) Tax Deduction Substantiation & Legal Evidentiary Record

- Roger Pay

- Jun 12

- 8 min read

LHDN Tax Deduction Substantiation Framework

LHDN Section 33(1) Tax Deduction Substantiation & Legal Evidentiary Record

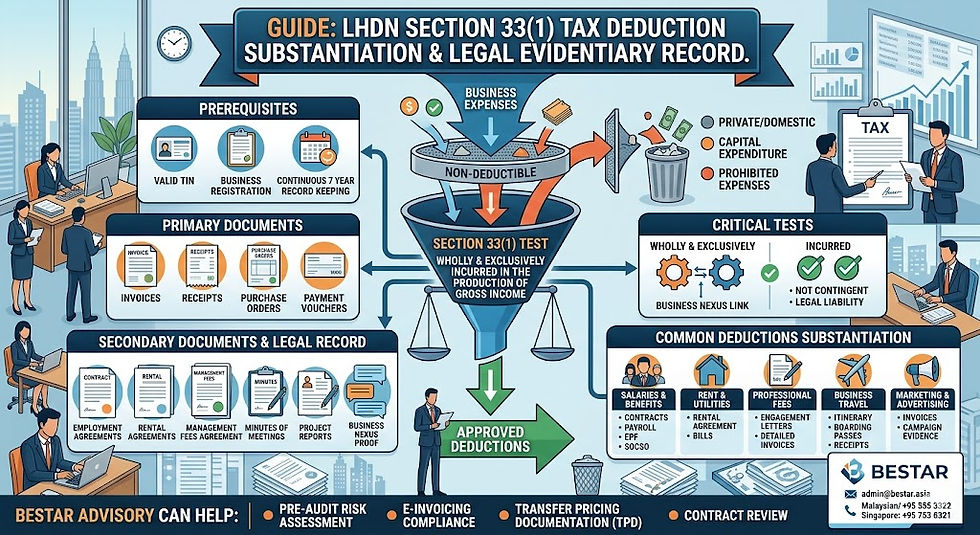

Under Section 33(1) of the Income Tax Act 1967 (ITA), the general rule for deductibility hinges on whether an expense was "wholly and exclusively incurred in the production of gross income."

However, passing the statutory definition is only half the battle. In modern LHDN (Lembaga Hasil Dalam Negeri) field audits and investigations, the survival of a deduction rests entirely on the quality and legal robustness of your evidentiary record. The burden of proof lies squarely on the taxpayer (Paragraph 13, Schedule 5, ITA).

The following framework outlines the legal standards of substantiation, statutory record-keeping mandates, and recent judicial precedents that dictate what constitutes an unassailable tax evidentiary record.

1. The Statutory Pillars of Section 33(1)

To build a defensible evidentiary record, every transaction must satisfy all four judicial tests inherent in Section 33(1):

[ Outgoing or Expense ]

│

( Must be Revenue, NOT Capital )

│

▼

[ Wholly & Exclusively ]

│

( Purposive Test: No Dual Substantive Purpose )

│

▼

[ Incurred ]

│

( Definite Legal Liability, NOT Contingent )

│

▼

[ In the Production of Gross Income ]

│

( Direct nexus to the income-generating nexus )

The Interplay with Section 39: Even if an expense fulfills Section 33(1), it will be retroactively disallowed if it falls under any prohibition listed in Section 39 (e.g., domestic/private expenses, non-approved funds, or capital-enhancing expenditures).

2. Core Legal Evidentiary Framework

A valid evidentiary record requires a multi-layered documentation strategy. Relying solely on accounting ledgers or a basic invoice is no longer sufficient during a modern tax audit.

A. Constructive Proof vs. Physical Evidence

LHDN routinely rejects retrospective documentation created after an audit notice is served. A contemporaneous, legally binding trail must be maintained for seven years (Section 82, ITA).

Expense Type | Primary Contractual / Legal Layer | Operational & Contemporaneous Layer |

Management Fees & Intercompany Charges | • Comprehensive Management Services Agreement (MSA) • Transfer Pricing Documentation (if applicable) | • Detailed time-sheets or time-cost allocations • Executive meeting minutes • Project deliverables / reports |

Subcontractor & Project Costs | • Principal Contract & Bill of Quantities (BQ) • Formally executed Settlement Agreements | • Approved Progress Claims & Architect/Engineer Certificates • Documented Variation Orders (VOs) |

Legal & Professional Fees | • Engagement/Retainer Letters • Detailed scope of work | • Itemized legal bills distinguishing between trade rights maintenance (deductible) vs. capital asset acquisition (non-deductible) |

Overseas / Business Travel | • Company Travel Policy • Board Resolutions (for executive travel) | • Boarding passes, itineraries, and written trip reports detailing specific business outcomes/income nexus |

3. High-Risk Vulnerabilities & Critical Judicial Precedents

Recent cases before the Special Commissioners of Income Tax (SCIT) and the High Court highlight exactly where taxpayers fail to substantiate their claims:

A. The Danger of "Sham" Agreements & Lack of Service Proof

Key Case: Multi Square Sdn Bhd v Ketua Pengarah Hasil Dalam Negeri (2021)

The Issue: The taxpayer claimed deductions for management fees paid to its holding company based on a brief, one-page agreement.

Judicial Takeaway: The High Court dismissed the appeal and deemed the agreements a "sham" because they were silent on execution details. They lacked metrics on how services were verified, the headcount involved, time costs spent, and liability terms. Without operational logs proving services were actually rendered, written contracts fail.

B. Mismatched Progress Claims & Structural Records

Key Case: GCSB v Director General of Inland Revenue (SCIT, May 2024)

The Issue: The taxpayer attempted to claim subcontractor expenses that failed to align or match mathematically with the actual progress claims and variation orders submitted to the revenue authority.

Judicial Takeaway: The SCIT confirmed additional assessments and penalties under Section 113(2). Amending ledgers or submitting retrospective settlement agreements during an audit was explicitly ruled an afterthought and legally invalid without original corroborating primary source documents.

C. Capital vs. Revenue Nature (Feasibility and Preparatory Costs)

Key Case: Sesco Bhd v Director General of Inland Revenue (SCIT, Feb 2023)

The Issue: Deductions were claimed for Feasibility Studies (FS) intended to explore new hydroelectric sites.

Judicial Takeaway: The court held that because the studies were geared toward creating or developing long-term physical assets, the expenses were capital in nature—violating Section 39(1)(c) and rendering them completely non-deductible under Section 33(1).

4. Minimum Substantiation Checklist for Audits

To ensure an evidentiary record withstands LHDN scrutiny, check that your documentation includes the following structural criteria:

[ ] The Seven-Year Rule: All primary source documents (invoices, receipts, bank statements, payment vouchers) must be archived securely for 7 years in an unalterable format.

[ ] The Specific Recipient Rule: For all commissions, contract payments, and rentals, records must explicitly capture the Name, Address, Identity Card/Passport Number, and Tax Reference Number of the recipient.

[ ] The Purpose/Nexus Test: Ensure that payment descriptions explicitly define the business activity being performed. Avoid vague descriptions like "For services rendered" or "General consulting."

[ ] The Execution Metric: For intercompany or advisory fees, maintain a rolling register of actual outputs (emails, presentations, sign-off sheets) to demonstrate that the transaction was fully executed in reality.

Would you like to examine the evidentiary requirements for a specific type of expense, like intercompany management fees or bad debt write-offs?

Would you like to review an example of an allocation key clause or discuss how LHDN audits management fees during a tax investigation?

How Bestar Malaysia Can Help

LHDN Section 33(1) Tax Deduction Substantiation & Legal Evidentiary Record

Navigating an LHDN tax audit in Malaysia has shifted from an exercise in accounting to a battle of legal and digital evidence. Under Section 33(1) of the Income Tax Act 1967 (ITA), proving that a business expense was "wholly and exclusively incurred in the production of gross income" requires far more than matching payment vouchers with standard invoices.

With LHDN enforcing Phase 4 mandatory e-Invoicing and utilizing advanced data analytics to flag anomalies, corporate tax deductions are highly vulnerable to retroactive disallowance. If your commercial substance, contract structures, or digital data fields contain even a minor mismatch, your business risks heavy penalties under Section 113(2).

As a premier corporate secretarial, accounting, and tax advisory firm, Bestar Malaysia provides specialized advisory services designed to transform your operational workflows into an unassailable tax evidentiary record.

The Strategic Importance of Section 33(1) Compliance

Section 33(1) is the bedrock of business tax deductions in Malaysia, but it is heavily guarded. To withstand an audit, every claimed expense must satisfy a multi-step judicial and administrative standard:

[ Outgoing or Expense ]

│

( Must be Revenue, NOT Capital Nature )

│

▼

[ Wholly & Exclusively ]

│

( Purposive Test: No Dual Private/Substantive Purpose )

│

▼

[ Incurred ]

│

( Definite Legal Liability, NOT Contingent )

│

▼

[ In the Production of Gross Income ]

│

( Direct nexus to the income-generating activity )

Failing just one arm of this test causes a domino effect. Even if an expenditure is genuine, LHDN will systematically disallow it if the contemporaneous documentation lacks legal substance or fails to match the real-time continuous transaction data now streaming to the MyInvois platform.

How Bestar Malaysia Protects Your Tax Deductions

Bestar bridges the gap between complex Malaysian tax law and your daily operational data. We build a comprehensive, multi-layered defensive shield for your corporate expenditures.

1. Navigating the Realities of e-Invoicing Compliance

LHDN's e-Invoicing mandate represents a significant structural change to tax substantiation. Under the current rules, standard paper or PDF invoices are no longer sufficient to support a Section 33(1) deduction.

The RM10,000 Individual Rule: For Phase 4 businesses operating under relaxation periods, consolidated e-invoices are permitted, but individual e-invoices are strictly mandatory for any single transaction of RM10,000 or above.

The 55 Mandatory Data Fields: Every transaction requires validated XML/JSON schemas containing accurate Tax Identification Numbers (TIN), product classifications, and digital signatures.

Bestar's Solution: We evaluate, upgrade, and align your accounting systems to interface directly with LHDN’s MyInvois API or portal. Bestar reviews your procurement structures to ensure every supplier invoice contains the exact structural data required. This prevents the immediate disallowance of your business deductions during an automated desk audit.

2. Formulating High-Risk Intercompany Management Fee Records

Intra-group expenses and regional management fees face intense scrutiny during LHDN audits. Under Section 140A and local transfer pricing rules, a deduction is completely vulnerable without a clear economic benefit analysis and a verified cost allocation model.

Bestar's Solution: We construct robust Transfer Pricing Documentation (TPD) tailored to local mandates, including Malaysia's narrow arm's length range (the 37.5th to 62.5th percentile). Bestar establishes a clear three-layer defense for intercompany charges:

Evidentiary Layer | Bestar’s Structural Deliverables |

1. The Legal Layer | Structuring comprehensive, contemporaneous intercompany agreements that explicitly define the exact scope of services and liability terms. |

2. The Economic Layer | Implementing defensible allocation keys (e.g., headcount, gross revenue ratios) and identifying local Malaysian comparable data sets. |

3. The Operational Layer | Implementing tracking workflows to secure "proof of life" evidence, such as cross-border emails, time-sheets, and executive meeting minutes. |

3. Preventing "Capital vs. Revenue" Reclassifications

LHDN field auditors actively target preparatory costs, project variations, and feasibility studies. They routinely attempt to reclassify trade expenses into non-deductible capital expenditures under Section 39(1)(c).

Bestar's Solution: Bestar's tax specialists conduct proactive pre-audit reviews of your contracts, project ledgers, and expense structures. By reviewing your documentation before submission, we ensure that recurring trade transactions are clearly differentiated from capital assets. This safeguards your deductions for ongoing business operations.

4. Maintaining the 7-Year Statutory Record Mandate

Under Section 82 of the ITA, the burden of proof rests entirely on the taxpayer to maintain unalterable, chronological business records for seven years.

Bestar's Solution: We help implement structured corporate secretarial and digital cloud accounting frameworks. This ensures all board resolutions, primary invoices, receipt archives, and validated e-invoices are stored in an organized, easily accessible format. If an LHDN auditor issues a surprise field notice, your company can produce a comprehensive evidentiary record instantly.

Secure Your Financial Position Before an Audit Begins

In the current tax environment, relying on an afterthought defense during an audit notice leads to costly adjustments and heavy penalties. True compliance requires proactive corporate planning, solid legal agreements, and seamless digital transaction data.

Partner with Bestar Malaysia to analyze your current risk exposure, implement correct e-invoicing workflows, and secure your corporate profits.

Explore how Bestar can optimize your local tax strategy:

Schedule a Section 33(1) pre-audit risk assessment

Align our business with Phase 4 e-Invoicing

Don’t Wait for an LHDN Audit Notice—Secure Your Deductions Today

The regulatory landscape under Section 33(1) and Phase 4 e-Invoicing leaves zero room for administrative or evidentiary gaps. Retroactive corrections are treated by LHDN as an afterthought, exposing your corporate profits to immediate adjustments, disallowed expenses, and severe financial penalties.

Protecting your business requires establishing a contemporaneous, legally sound, and digitally compliant transaction trail before field auditors flag an anomaly.

Partner with Bestar Malaysia to Fortify Your Tax Defense

Bestar’s team of corporate corporate secretarial, tax advisory, and transfer pricing specialists will help you structure your operations to survive the highest levels of tax scrutiny.

Pre-Audit Substantiation Reviews: We evaluate your contract frameworks, intercompany management agreements, and operational "proof of life" documentation to proactively identify and resolve tax risks.

e-Invoicing Alignment: We transition your continuous transaction workflows to satisfy LHDN's 55 mandatory data fields and digital signature validation protocols.

Transfer Pricing Documentation (TPD): We build compliant local benchmarking models tailored specifically to Malaysia's strict and narrowed arm’s length ranges.

Take Action Now

Don't let unverified corporate expenses become a significant tax liability. Schedule an introductory advisory consultation with our professional desks in Kuala Lumpur or Singapore to review your current Section 33(1) substantiation strategies.

Comments